Editor’s Note: This is the first in a series of articles based on an over-lunch interview with Case IH’s North America’s Jim Walker, Vice President, and Melinda Griffin, Director, Network Development, at the headquarters offices last fall in Racine, Wis.

Jim Walker

Last year was a challenging year for virtually everyone in the farm economy, but Case IH dealers as a whole saw unusually high challenges due to being exposed most heavily on the cash crop business, says Jim Walker, Vice President, Case IH North America, Racine, Wis. Compounding the rough business climate was the fact that Case IH was bringing change to its contractual agreement with dealers. As the saying goes, folks are all for change when it happens to somebody else. But when it’s being forced upon us, the first move can be clenching a fist.

The frustration from the red dealer network was heard by management in Racine, and also shown again in the results of the Equipment Dealers Association Dealer-Manufacturer Relations Survey, which was distributed to dealers early in 2017, completed in early winter and reported at mid-year. When published, the survey didn’t reveal anything that the manufacturer didn’t already know, Walker says, though the degree of scoring revealed frustrations in dealers’ business. Most of the elements of the new plan hadn’t been out long enough to have impacted dealers’ views in February of last year when the surveys were completed.

Click to enlarge.

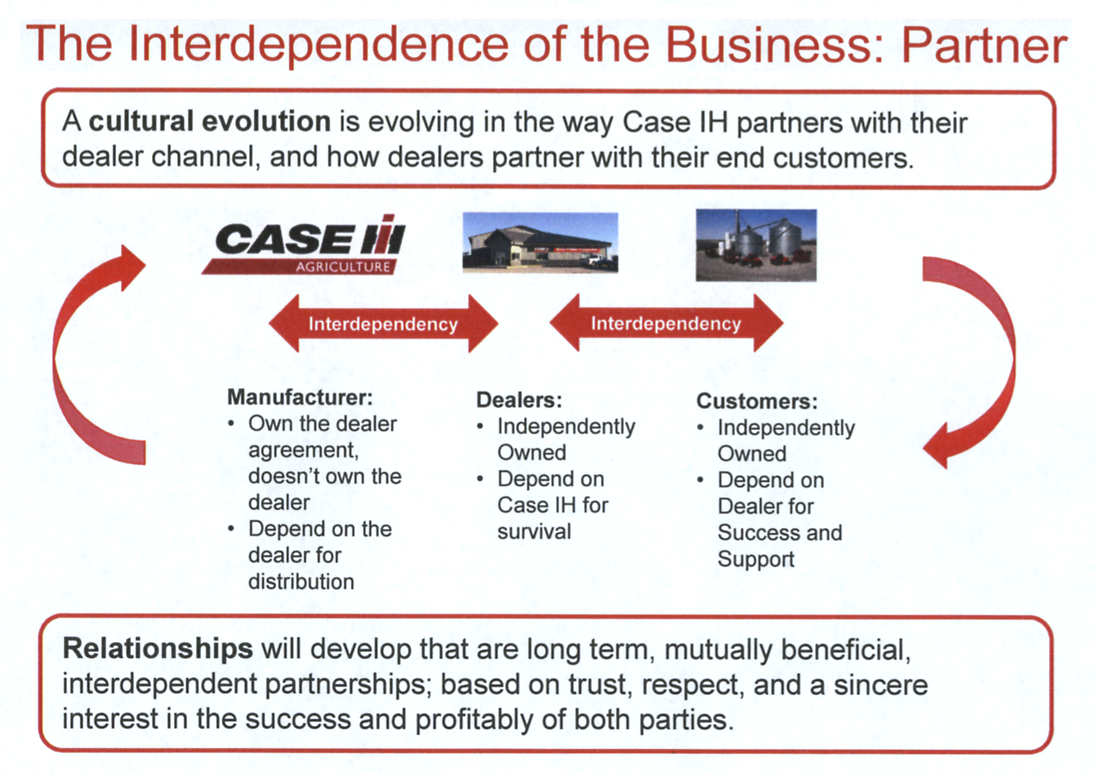

Just minutes into the meeting, Walker jumped right into the slide which was titled, “The Interdependence of the Business: Partner.” It was part of a presentation that was first shown at the annual dealer meeting 2 years earlier, and has since been incorporated into the larger strategic plan. “It depicts how we feel the relationship exists from the Case IH standpoint,” he says. “As a manufacturer, we own a dealer agreement, but we don’t own the dealer.”

It didn’t take long to introduce to elephant in the room, the new dealer agreement that got so much attention during the last couple of years. It was time for an update, says Walker, noting that the same agreement was used for 20-plus years as the world changed around everyone.

“That dealer agreement is a document that we hope puts in place a contractual relationship of obligations of both parties. It should be mutually beneficial, not used as a stick but as a protection of the investments both parties are making — like us as a manufacturer or a dealer that is investing in buildings and those types of things.”

While dealers remain independently owned, he notes that many depend on their full-line manufacturer for their survival. “When such a high percentage of their revenue comes from Case IH products, we have to respect that and be cognizant of the fact that we are their well-being at the end of the day. So if we’re working with that type of partnership or respect, they understand we need a new dealer agreement, we haven’t had one for a while.”

Walker said that the new agreement was in the works for about 5 years. “We aimed to have as much uniformity as we could between our different brands, so New Holland, Case CE and Case IH — that was the first driver. The second was to get everyone updated to that new agreement. We had the Tyler acquisition of sprayers, we’ve had different movement within our product ranges and it was just the right time to start at 4-5 years ago.

"Each year, we plan to compare actual results to the milestones of the strategic plan and make any adaptations necessary that might have surfaced from the previous year. In a 2018 update to the CIH Strategic Plan, the company has added the objective 'to deliver a best in class overall dealer-manufacturer relationship.'"

— Jim Walker, Vice President,

Case IH North America

Melinda Griffin, Director of Network Development, added that even though dealers knew well in advance that a new agreement was coming, it still made waves. “There’s only so much you can do to make a dealer feel comfortable with an agreement. But we met with the dealer associations and with the Dealer Advisory Board, and we made over 30 adjustments. We didn’t change everything thing that they asked, but we made 30 modifications based on that feedback.”

Walker adds that Griffin and her team in the field had steadily been getting dealers’ signatures as the end of the year deadline approached, but that it also happened quickly in some cases when an occurrence, like a change in ownership, an acquisition that will trigger a dealer agreement to be signed.

Pointing to the schematic in the slide, he described the dealer’s central role all of the business. “The customers are also independent and need a dealer. And yet they have choices of brands and even different dealers of the same brand. The business model of the ag industry has pressures on both sides of the dealer. The dealer has a manufacturer he absolutely depends on in Case IH, but understands he owes some obligations, too. He’s working with a customer base that can do business anywhere they want, but he has to have their revenue to be able to survive. So, it’s a precarious position to be a dealer in the ag business, and the capitalization that it requires.”

The Run-Up to 2017

While much of the conversation discussed the strategic plan that was rolled out in January of last year, Walker also described what preceded it. “From 2006 to 2013 we as Case IH North America were heavily engaged and involved with our dealer network side by side — with 2 out of 3 employees being located in the field. And we were really retail focused during this escalation of the industry and the upturn. But when things [deteriorated in the market] 2014 through 2016, we were in a wholesale mode.”

He said Case IH, like the other OEMs, scaled back production as far as it could to still produce competitive priced units. “Our focus during that period was wholesale focused and our retail focus was used machinery. And we transitioned into making sure that we had programming — we understood the dealer’s plight — on used machinery, and we drove that way. Dealers talk about the Partnership Program we had, whereas we said, ‘we’ll help you on your end of it with used machinery and even the new, but we need a sustainable level of orders from you to make sure that we’re running at an efficient quality level at a competitive price.’”

Some dealers took the Partnership Program well, others didn’t. But the need for partnering was understood, he says.

Walker and his team were encouraged with what was happening in Canada in the second half of 2016, and the market had taken off for high horsepower products. He says Case IH knew that 2017 in the U.S. would still be challenged on the cash crop side, and still “hand to mouth,” but that it would no longer be facing the double-digit declines.

“So we worked on a strategic plan that would be based on how we could, at the bottom of all of this, gain sustainability moving forward. The things we would put in place would work for us not just during an upturn but also during the downturn and ag’s future cycles.

Case IH introduced the strategic plan in the early winter of 2017 and held 6 regional meetings, in which every dealer-principal in those regions was invited. “We wanted it to be kind of a town hall discussion on the strategic plan and we opened ourselves up and took Q&A.”

Among the visuals was a slide titled “Case IH Strategic Plan: Core Strategies.” The 5-item* list consisted of:

- Improve customer product experience

- Enhanced dealer business interface

- Achieve alignment with dealers

- Focus on dealer capabilities and health

- Deliver sustained market share growth

In reviewing the core strategies, Walker said the first is clearly based on quality of product. “The next 3 are all based on dealer network from the standpoint of whether we’re in alignment with them, whether they’re healthy, whether they’re able to drive and grow the business. Our whole sustainability is based on that dealer network that we talked about.”

Something Walker wanted to discuss was the differences in Case IH’s networks than some of the others, which showed up in the industrywide survey results. “What our Case IH dealers have been going through unfortunately in this downturn, which was primarily driven by cash crop, was a market down 65% on high horsepower products and 75% on planting. Our dealer network is predominantly cash crop network in North America. It’s a full line of product offering, but it’s a cash crop network. They derive the majority of their revenue from Case IH cash crop products.”

He noted that Deere’s model has a distribution network with a balanced of product offering, something AGCO also accomplished with its different brands, including Hesston, Sunflower and Challenger.

“Unfortunately this downturn of cash crop probably magnified the financial effect on our dealers more so than competition. So our dealers are in this position of being more adversely affected. Their strength of product support business has been growing, which we all know is very important, but probably not near the level that they would like for it to be to say that it’s a stable base that they have in revenue.”

* Since the meeting and discussions of the CIH Strategic Plan, Walker said an additional objective has been added to the mix. Walker told Farm Equipment in late January that the company compares actual results to milestones of the plan each year, and makes any adaptions that might have surfaced from the previous year. Walker notes the 2018 update to the Strategic Plan now includes a 6th objective ... “to deliver a best-in-class overall Dealer-Manufacturer Relationship.”

Read more in the Case IH Dealer Network Series Update >>

Coming Next … Future installments in the series cover Dealer Incentives, Dealer Advisory Board & Communications; Competing Brands and New Resources in Best Practice Sharing.