(Editor's Note: This interesting take on Kubota acquiring Norwegian farm implement maker, Kverneland, was apparently published prior to CNH announcing that it, too, was submitting a bid for the company. Nonetheless, Dr. Scholl's comments are interesting as they relate to the valuation of Kubota's bid. He also discloses that he is "long Kverneland Group ASA and has been a shareholder since 2009.)

The plight of the Japanese exporter can not be overstated. Over the last five years, the Japanese yen has been rising steadily against most major currencies, appreciating by about 50% over the past five years against the US dollar and the euro. This causes severe problems for Japan-based manufacturing into export markets, especially automobiles and machinery. Just a week ago, Toyota Motor (TM) had to slash its earnings guidance by half, one of the reasons being the strong Faced with a stagnant domestic demand, Japanese corporations have been seeking foreign takeovers to counter these difficulties. Here, the strong Yen is a great help and enables Japanese corporations to buy out companies in euros or dollars with their strong currency. Recent notable examples include the 10bn euro takeover of Nycomed by Takeda Pharmaceuticals (TKPHF.PK) earlier this year or the $4bn takeover of Brazilian brewer Schincariol by Kirin (KNBWY.PK).

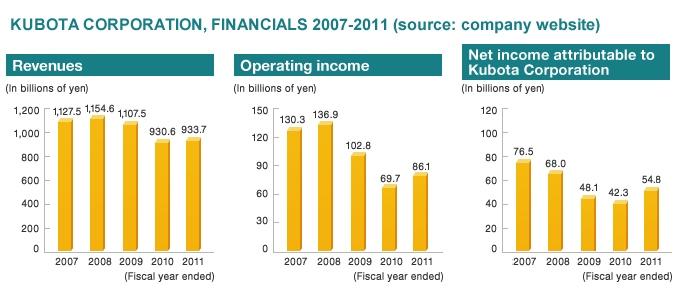

The Japanese farming machinery, water systems and infrastructure company Kubota Corporation (KUB) announced a similar deal last Friday. Kubota plans a tender offer for all shares of the Norwegian farming equipment maker Kverneland Group (KVEGF.PK), valuing the company at NOK 8.50 per share, about $220m or 17 billion yen. This is not a huge amount for Kubota, which had on average a trillion yen in yearly revenue over the past years, and the sum represents less than a third of last year's net income.

However, Kubota will very likely make an excellent deal with this acquisition. Not only is it buying an asset in a foreign currency with a strong yen (the yen has appreciated 45% against the Norwegian krone over the past five years), but it is buying a strong and reputed brand in the agricultural space for a very attractive price. The NOK 8.50 that Kubota is offering may be a good premium to the recent share price of Kverneland (the stock was up 34.5% on Friday), but if you look at the prices at which the share has been trading over the last decade, you can see Kubota is really making a bargain purchase here (see chart). This is definitely not the type of overpriced takeover that Olympus Corporation (OCPNY.PK) used to hide its decade-old losses.

Kverneland is well-known in the farming community for its ploughs, seeding equipment and fertilizer spreaders. Basically, Kverneland is manufacturing all kinds of farming equipment that is trailed by a tractor, while Kubota is building the tractors. That looks like a great fit. Furthermore, Kubota is one of the leading manufacturers of equipment for paddy farming (rice combines and harvesters, strong market position in Asia), and the upland farming equipment of Kverneland will enable it to access the complementary market of upland farming. It will also allow Kubota to diversify its geographical revenue (90% of Kverneland's revenue comes from Europe, Nordic countries, central Europe and Russia) and production bases. Kverneland's extensive distribution network and relationships with farmers will also be of value to Kubota to distribute its own tractors. Kverneland makes about eur 400m in revenue yearly (after the divestment of the bale equipment business to Bucher in 2009), with a gross profit margin of about 45%. Much of its gross profit has been eaten up in the past years by SG&A and other costs, which have prevented Kverneland Group from posting meaningful profits. The Japanese will likely streamline the business and be able to extract synergies from the merger.

All in all, Kubota shareholders can be very happy with this deal, which is nearly certain to be completed since the main shareholder of Kverneland already approved the offer. Kubota shareholders have little reason to complain, as the company has performed very well over the last decade, rising more than 180% in US dollars (and paying dividends on top), compared with a 250% rise in the price of shares of its US rival John Deere (DE), and a 23% rise in shares of Fiat associate CNH global (CNH).

As a Kverneland shareholder, I would have preferred an exchange offer in shares to participate in the upside of the parent – but as I explained in the beginning, Japanese corporations want to use the advantage of their strong yen, and they pay cash.

Dr. Clemens Scholl was born in Salzburg, Austria. He went to school and high school in the french-speaking part of Belgium, studied physics and mathematics at the University of Cologne, Germany. He obtained a PhD in nuclear physics magna cum laude, and conducted experimental research at several national and international accelerator facilities. He has published a large number of academic papers in the field of experimental nuclear physics. Dr. Scholl has lived in Austria, Germany, England, Belgium, France and Japan. He currently lives in Germany.