A year ago in the 2024 Dealer Business Outlook & Trends Report, dealers indicated 2024 would be the toughest year for business since the COVID-19 pandemic. The results of the latest survey suggest that the same can be said for 2025.

Coming off a year where dealers had to battle lower commodity prices, increasing costs for equipment and inputs, the uncertainty of an election year and high new and used equipment inventory, the outlook for 2025 revenues skews negative with the lowest percentage of dealers forecasting new equipment revenue growth seen in over a decade.

For the second year in a row, the survey saw a drop in optimism in dealers’ new and used wholegoods revenue forecasts. While dealers are still forecasting revenue growth for parts and service, the percentage dropped from the record highs seen in the 2024 report.

Low Dealer & Farmer Sentiment Continues

Dealer and farmer sentiment continues to remain low, as it has for the past two Dealer Business Outlook & Trends reports. Gone are the days of low sentiment because of supply chain issues and low inventory levels. Much like in the 2024 report, dealer sentiment has been low throughout the year due to declining sales, high interest rates and increasing costs of equipment.

In Ag Equipment Intelligence’s latest Dealer Optimism Index, net dealer optimism came in at –43%, the lowest optimism reading in 2 years (tied with August 2024). In the latest reading, 3% of dealers reported being more optimistic in October than they were the previous month, while 47% of dealers reported being less optimistic than the month before.

Dealers continue to point to low farmer sentiment as a factor impacting their sales and outlook. One Corn Belt dealer said, “Demand continues to be softer than expected. We feel like farmer sentiment will be depressed heading into 2025 with sales likely down an additional 10%+ year-over-year (YoY).”

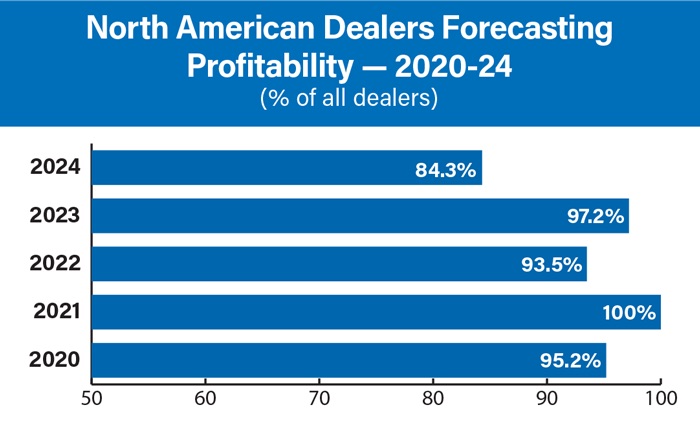

Dealers forecasting profitability fell to a 5-year low in 2024, with 84.3% of dealers saying they’ll be profitable vs. 97.2% in 2023.

Another dealer noted that buyer hesitation is growing each month as profitability deteriorates. Another said, “Commodity market values are below production costs, ultimately limiting sales.”

Inventory Challenges. New equipment inventories continue to be a challenge for dealers. However, in terms of dealers’ top concerns for 2025 it falls to the middle of the pack at No. 12 (up two spots from No. 14 in the 2024 report). According to the latest Dealer Sentiments Report, a net 75% of dealers report their new equipment inventories were “too high” (76% too high, 22% in line, 2% too low) in October, vs. a net 70% reporting inventories were too high the month before.

The picture is a little better on the used equipment side, with a net 35% of dealers saying their inventory was “too high” in October (43% too high, 48% in line, 8% too low). This was up for a net 23% of dealers who said their used equipment inventory was “too high” in September.

“We are surprised by the amount of OEM involvement in managing dealer inventory levels. The collaboration is essential in ensuring inventory levels become right sized in 2025 across product lines and locations,” said one Corn Belt dealer.

Pricing. In the October Dealer Sentiments Report, price contribution was reported down about half a percent on average vs. flat in September. This was the first negative reported price contribution since June 2020. Commentary suggests the rate of incentive programs has accelerated in recent months as farmer sentiment and end user sales have deteriorated with programs varying from financing, warranty, parts and service, etc.

Dealers reported used equipment pricing was down 6% year-over-year in October vs. down 4% the month prior. Most pricing pressure was on combines, followed by high horsepower tractors.

By equipment segment, used combine prices were down 11% year-over year in October, used 4WD tractors pricing was down 5% and used high horsepower tractor pricing was down 6%. Used compact and utility tractor pricing was down as well at –5% and –3%, respectively.

Customer Concerns. While dealer sentiment took a dip in October, the latest Ag Economy Barometer from Purdue Center for Commercial Agriculture released Dec. 3, 2024, shows farmer sentiment had a boost post-election climbing to 30 points from October to 145.

The biggest driver of the sentiment improvement was an increase in producers’ confidence in the future, as the Future Expectations Index jumped 30 points to 124. The Current Conditions Index also rose in October but by a smaller amount. “With a reading of 95, the Current Conditions Index confirmed that farmers think economic conditions this year are worse than last year and weaker than during the barometer’s base period of 2015-2016, which was in the early days of a multi-year downturn in the U.S. farm economy,” noted James Mintert and Michael Langemeier, the report authors. “Producers this month expressed some optimism that economic conditions will improve and not precipitate an extended downturn in the farm economy.”

Learn More Online

The full 2025 Dealer Business Outlook & Trends report is available here!

Mintert and Langemeier also noted that farmers are feeling better about the future of the U.S. ag economy and have a less pessimistic view. “For example, the percentage of producers who expect bad times for the U.S. agricultural economy in the upcoming year declined from 73% of respondents in September to 53% in October. Similarly, the percentage of producers who expect bad times for U.S. agriculture in the next 5 years fell from 48% to 33%,” they said.

Looking ahead to 2025, higher input costs ranked highest among farmers’ biggest concerns for their farming operation next year, with 34% ranking that as their top choice. This was followed by lower crop and/or livestock prices (30%) and rising interest rates (15%).

The Farm Capital Investment Index saw an improvement in November at 55 up 13 points from October after a 7 point increase from September, which Mintert and Langemeier said is “another signal that producers in October might be viewing 2024’s weak income prospects as transitory.”

2025 Wholegoods Outlook

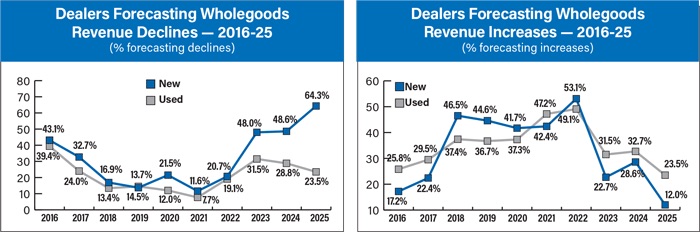

New wholegoods revenue projections were once again largely negative. Over two-thirds of dealers (64.3%) are forecasting new equipment revenues to be down at least 2% in 2025. This compares to 28.8% who forecast a decline for 2024, and is more than double the percentage of dealers forecasting a decline for 2023 new equipment revenue. The last time at least half of dealers were forecasting new equipment revenues to decline was in 2015. That year, when 50% of dealers forecast their new equipment sales would be down at least 2%, North American row-crop tractor and combine unit sales were down 25.9% year-over-year.

About a quarter of dealers are forecasting their new equipment revenue to be flat in 2025, while 12.4% predict revenue from new equipment sales will be up at least 2% in the year ahead.

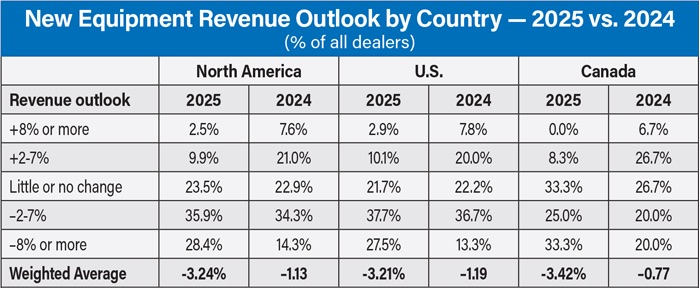

By country, U.S. dealers were less optimistic about new equipment revenue growth in 2024, with 13.0% expecting an increase of 2% or more vs. 8.3% of Canadian dealers.

In the U.S., 13.0% of dealers are projecting new equipment wholegoods revenue to be up at least 2% in 2025, while 21.7% of U.S. dealers are expecting revenues to be flat. Looking at U.S., dealers are forecasting a decline in new wholegoods revenue, as 37.7% are expecting a 2-7% drop and 27.5% are expecting revenues to be down 8% or more.

In Canada, just 8.3% of dealers expect new equipment revenues to be up at least 2% in 2025. But more Canadian dealers than U.S. dealers are projecting new equipment revenues to be flat at 33.3%. A quarter of dealers in Canada are forecasting new equipment revenue to drop 2-7% in 2025 and a third expect revenues to be down 8% or more.

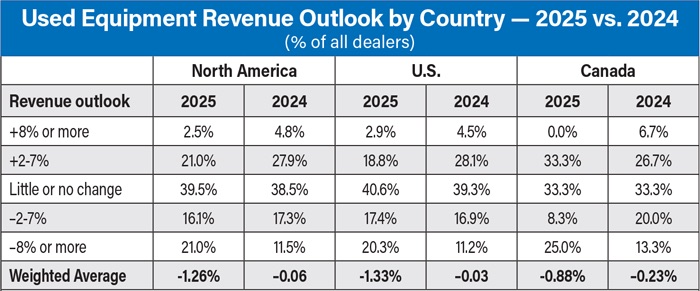

The used equipment revenue forecast picture is slightly more positive looking to 2025. Nearly a quarter of dealers (23.5%) anticipate their used equipment revenue will increase by 2% or more vs. 2024. About 40% of dealers forecast their 2025 used equipment revenue will be about the same as this year. When it comes to declining revenues, 37.1% of dealers are forecasting used equipment revenues will fall vs. this year.

Nearly 22% of U.S. dealers are expecting some level of revenue growth from used wholegoods in 2025, while 40.6% are calling for revenues to be flat. About 17% of U.S. dealers are expecting used wholegoods revenues to be down 2-7%, and another 20.3% are calling for revenues to be down 8% or more from used equipment.

More Canadian dealers are forecasting revenue growth in their used equipment revenue for 2025 at 33.3% vs. 21.7% of U.S. dealers saying the same.

Canadian dealers are more positive on used equipment wholegoods with two-thirds projecting revenues to be as good or better than in 2024 (33.3% up 2-7% and 33.3% flat). But, a quarter of Canadian dealers are calling for used equipment revenues to be down 8% or more.

The good news for 2025 revenues will come from the aftermarket side of the business. The majority of dealers forecast parts and service revenues to be as good or better than 2024. Notably, over 90% of dealers say their service revenue will be as good or better (42.0% flat, 43.2% up 2-7% and 7.4% up 8% or more).

Dealers in the U.S are fairly in line with the North American forecast, with 7.3% calling for service revenues to be up 8% or more and 40.6% expecting a 2-7% increase in revenues. Just shy of 45.0% of U.S. dealers expect little or no change in their service revenues for 2025 compared to 2024. In terms of declining revenues, 5.8% of U.S. dealers expect a drop of 2-7% while just 1.5% of dealers are forecasting declines of 8% or more for service revenues.

Dealer 2024 Revenue & Gross Margin Estimates vs. Forecasts

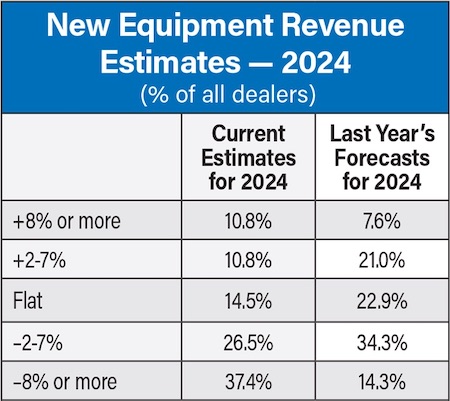

At the time of last year’s survey, 48.6% of dealers forecast their new equipment revenues would be down in 2024 compared to 2023. With the year coming to a close, that percentage has grown, by just over 15%. In the latest report, 63.9% of dealers report their new equipment revenues will be down in 2024 vs. 2023. This stands to reason, as the October 2024 AEM unit sales numbers show that North American row-crop tractor sales are down 36% year-to-date and combine unit sales are down 32% year-to-date.

Dealers were more optimistic about 2024’s results when they made their forecasts last year. Now, over 60% of dealers estimate their 2024 new equipment revenues will be down at least 2% vs. 2023.

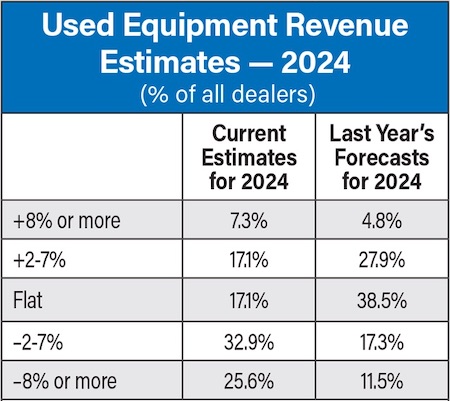

Over half of dealers expect used equip- ment revenue to be down vs. 2023 compared to the 28.8% who forecast a decline for 2024 in last year’s survey. Nearly a quarter of dealers did report used equipment revenue was up.

Looking at used equipment, a year ago 32.7% of dealers were expecting revenues to increase over 2023. Reflecting on the year today, 59.5% of dealers say their used equipment revenue will be down vs. 2023.

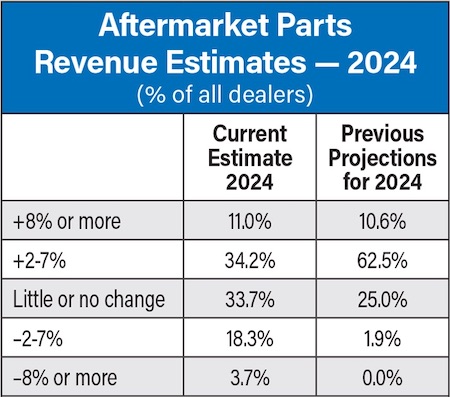

While the majority of dealers parts revenue was up in 2024 vs. 2023, dealers didn’t quite hit their estimates from a year ago.

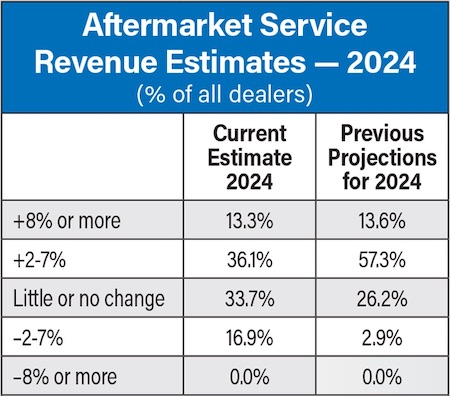

Dealers reported the best results in service revenue vs. 2023 and were not too far off from their forecasts for the year.

On the aftermarket side of the business, dealers’ forecasts for 2024 came closer to how the year is panning out. While the majority of dealers are reporting revenue growth for both parts and service vs. 2023, the percentage reporting growth is lower than those who forecast growth last year. For service, last year 70.9% of dealers fore- cast their revenue would be up at least 2% vs. 2023, compared to 49.4% who report their 2024 service revenues are up at least 2% over 2023. The picture is similar for parts revenue. Last year, 73.1% of dealers forecast their parts revenue would be up at least 2% vs. 2023. Today, 45.13% of dealers say their parts revenue is up at least 2% over 2023.

While the year didn’t turn out how dealers forecast, 84.3% of dealers report they will be profitable in 2024.

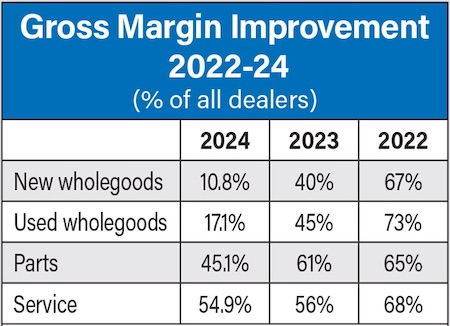

The percentage of dealers reporting improvements in their gross margins was down year-over-year for 2024 in all categories.

Canadian dealers are more positive on service revenues than their counterparts in the U.S., with 58.3% calling for an increase of 2-7% vs. 2024. Another 8.3% say their service revenues will be up 8% or more in 2025. Meanwhile, a quarter of Canadian dealers expect flat service revenues form2025. Just over 8% of dealers in Canada expect service revenues to be down 2-7%, and no Canadians are projecting service revenue to be down 8% or more.

Turning to parts revenue, it’s a similar picture with 43.2% of dealers projecting flat revenues, 44.4% forecasting growth of 2-7% and 4.9% expecting revenues to be up 8% or more. Just 7.4% of North American dealers are projecting parts revenue to be down 2-7% and no dealers said they expect declines of 8% or more.

In the U.S., about 45% of dealers are forecasting parts revenue to grow 2-7% over 2024, and 4.4% expect revenues to wbe up 8% or more. Additionally, 8.7% of U.S. dealers expect parts revenues to drop 2-7% and the remainder (42.0%) are calling for parts revenue to be flat vs. 2024.

In Canada, no dealers are calling for parts revenue to be down compared to 2024. While half are calling for flat revenues, 41.7% forecast parts revenues to grow 2-7% and another 8.3% of Canadian dealers expect revenues to increase 8% or more.

Equipment Prices & Early Orders

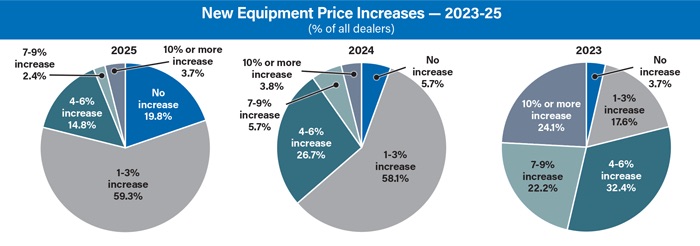

Just over 80% of dealers expect a price increase from their mainline supplier in 2025, down from 94.3% in the last report. Dealers expecting a price increase of 10% was about even with 2024 at 3.7%. In the 2023 report, 24.1% of dealers said they expected a price increase of 10% or more from their OEM.

The highest percentage of dealers (59.3%) are expecting a 1-3% price increase from their OEMs, which is up slightly from last year when 58.1% of dealers said they expected this level of increase. Just shy of 15% of dealers say they expect their OEM to raise prices by 7-9%. And, almost 20% of dealers are not expecting a price increase from their mainline supplier in 2025.

19.8% of dealers are forecasting no new equipment price increases next year, the highest percentage in the last 3 years.

Less than 5% of surveyed dealers reported an increase in early orders for 2025, down from 15% in 2024. Another 17.1% of dealers report their early orders are about the same as 2024 vs. 29.0% who said their early orders were flat in the last report.

Just over 78% of dealers said their early orders were down to some degree vs. 2024. Breaking it down, the highest percentage of dealers (36.6%) said their early orders were down more than 10% vs. the year before, compared to about 15% who said the same in the 2024 report.

The dealers who said early orders are down 6-10% increased as well at 19.5% vs. 16.8% in 2024. Dealers who reported early orders were down 1-5% dropped from 24.3% in 2024 to 22.0% in 2025.

Dealers Expect Declining Tractor & Combine Sales

Overall, dealers’ outlook for tractor and combine unit sales leaned negative. 4WD tractors had the highest percentage of dealers forecasting some level of unit sales growth at 12.5%, followed by <40 horsepower tractors at 11.8% projecting unit sales growth of 2% or more.

All 4 tractor categories saw double-digit declines in the percent of dealers forecasting unit sales growth in 2025. The largest drop was for high horsepower tractors. For 2025, 10.5% of dealers forecast unit sales to be up at least 2% vs. 29.7% who said the same for 2024. High horsepower tractors also had the highest percentage of dealers forecasting unit sales to decline 2% or more (50.0%).

For combines, just 7.7% of dealers are forecasting unit sales to increase in 2025 vs. 13.2% in 2024. Almost two-thirds (63.1%) of dealers are expecting their combine unit sales to be down 2% or more in 2025.

Best Bets for Increasing Sales

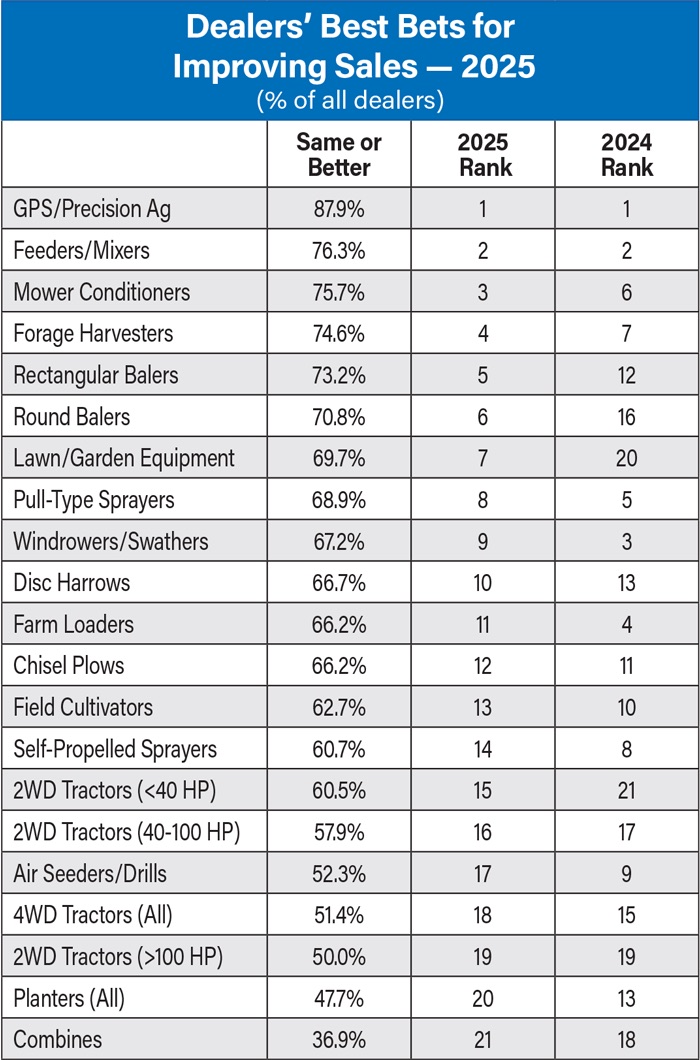

Each year dealers are asked to provide their unit sales projections for a number of product categories. Those projections are used to determine dealers’ best bets for improving sales in the year ahead. For the second year in a row, GPS/Precision Ag topped dealers’ list of best bets for improving unit sales, with 87.9% of dealers forecasting sales to be as good or better than 2024.

Precision farming systems and feeders/mixers maintained the top 2 spots for dealers’ best bets.

With grain prices continuing to remain low, dairy provides a bit of optimism for equipment sales for dealers and manufacturers alike. The “best bets” list confirms that livestock and dairy customers will provide opportunities for dealers in 2025. No. 2-6 all fall into the hay & forage product segment — feeders/mixers, mower conditioners, forage harvesters, rectangular balers and round balers. Feeders/mixers were No. 2 in 2024 as well, but the others all were up over last year. Rectangular and round balers saw the largest jump — moving from No. 12 and 16, respectively, to No. 5 and 6.

Rounding out the top 10 are lawn/garden equipment, pull-type sprayers, windrowers/swathers, and disc harrows. Finishing at the bottom of the list were planters at No. 20 and combines and No. 21.

Top Concerns

While interest rates have been a hot topic for all of 2024, interest rate increases fell down to the #8 ranked concern for 2025 after topping the list for 2024. Dealers ranked 22 different issues and concerns, with rankings determined by the percentage of dealers that are both “concerned” and “most concerned.”

Taking the top spot this year was the increasing cost of new equipment — up from #4 last year — with 68.0% percent of dealers saying they were “most concerned.” Technician availability held steady in the #2 spot for the 6th year in a row. Tied at #2 were farm input costs and farm commodity prices. The shrinking farm customer base rounded out the Top 5, with 46.2% of dealers saying they were “most concerned” with this issue, up from #8 last year.

Given that dealers are reporting their new equipment inventories are too high, it was somewhat surprising that new equipment inventory came in at the middle of the pack at #12, up from #14 last year. Used equipment inventory dropped a ranking to #14. The bottom of the list remained pretty consistent with 2024. The bottom 5 include: dealer consolidation (#18 last year), dealership “purity” efforts by the majors (#20 last year), labor regulation (#16 last year), business loss from right-to-repair (#21 last year) and manufacturer consolidation (#22 last year).

Hiring & Investments for 2025

By and large, dealers aren’t planning much change in their employee numbers for 2025. With the exception of service technicians, the majority of dealers responded “no change” for the other positions. Just over 67% of dealers said they were planning to hire service techs in 2025, down from 84.8% who said the same for 2024. The parts department presented the next biggest need for employees, with 25.3% of dealers saying they would be hiring in the parts department, again down from 2024 when 45.7% of dealers were planning to hire for the department.

Corporate/administrative roles were the least likely area for dealers to hire for 2025 (7.7%), and had the highest percentage of dealers (14.1%) who said they planned to reduce staff.

Nearly two-thirds of dealers say they won’t increase their capital spending vs. 2024. Just shy of 27.0% of dealers plan to increase their capital spending by up to 5% over 2024 and 7.7% say they’ll increase spending by 6-10%. No dealers are planning to increase spending by 11% or more.

In terms of where dealers will invest in 2025, once again shop & service had the highest percentage of dealers planning to invest there at 31.7%, but this is down from 62.9% in 2024. Another 30.3% of dealers said they are investing in mobile service vehicles vs. 48.5% in 2024 and 57.0% in 2023.

Dealers planning to invest in business information systems dropped to 22.4% from 36.7% in 2024 and 42.3% in 2023. The percentage of dealers planning to invest in their retail space and showroom dropped by more than half to just 15.8% for 2025.