Getting a handle on the current financial landscape of the farm equipment industry is critical for establishing meaningful benchmarks and insightful comparisons for any dealership. Produced by Equipment Dealer Consulting LLC, the comprehensive financial and operational analysis presented in the North American Equipment Dealers Assn. (NAEDA) “Cost of Doing Business Study 2024” helps equip dealers with straightforward guidelines to assess the profitability of equipment dealerships spanning all brands across the U.S. and Canada. The findings are valuable in helping to unravel financial trends, optimize operations and propel dealerships toward heightened success.

NAEDA’s CFO Curt Kleoppel, CPA, CVA and president of Equipment Dealer Consulting LLC says over the years NAEDA has used the study to advocate on behalf of dealers in significant ways: helping enact floorplan interest deductions and other tax regulations; establishing industry-specific targets and benchmarks; assisting in valuing dealerships for mergers/acquisitions and buy/sell agreements; and strategic estate planning.

The study produced 6 total reports, different from last year, but all including 2024 and 2023 data including: OPE Specific; Sales Volume Categories; North America; Canada; USA; Regional.

“There’s quite a bit of data in this year’s study,” Kleoppel says, adding, “This year, we changed it up quite a bit, as we think these bracket volume categories suit the business environment going forward. We’re seeing a lot more expansions, mergers, acquisitions, and the dealerships are getting bigger. It’s possible for next year’s study for 2025 that we’ll add the $1B category.”

5 Key Facts About the Study

- Published annually by the North American Equipment Dealers Assn. (NAEDA), sponsored by Fusable.

- Assesses the financial performance of equipment retailers who submit their confidential financial reports to the Equipment Dealer Consulting LLC accounting team.

- Designed to provide comprehensive, straightforward guidelines for analyzing the profitability of equipment dealerships, serving as a valuable tool in understanding the equipment dealer industry and operational information to help dealers improve their business. The report is available free of charge to all NAEDA members.

- Made possible through the cooperation of participating dealer associations and their equipment dealers who provide detailed financial and operational information for their individual companies. Questionnaires were mailed to all dealers in the participating association territories.

- Offers the following: balance summary; income summary; ratio summary; observations; balance sheet; income statement; employee count; financial ratios; trend analyses. Also provides: balance sheet, income statement, employee count and financial ratios all by sales volume.

For this year, comparing changes for the different volume size dealerships was analyzed for three categories: sales less than $50M; sales between $200M-$600M; and sales over $600M. For the purposes of this overview, Farm Equipment is focusing on the latter two categories.

(Note: The fourth category from the prior year, sales between $50M and $200M, is included in the study; 2023 numbers were recalculated by moving those financials from last year’s categories to fit into the new categories for this study).

Another change from last year is that averages are per entity basis. Trent Hummel, a former dealer executive and a NAEDA Dealer Institute instructor based in Canada who presented an overview of the study with Kleoppel during a Farm Equipment webinar analyzing the study, says this was a welcomed improvement, as it offers a much easier way of looking at the data.

The average number of locations per organization was 9.3 in 2024, compared to 7.2 in 2023. There are many locations with more than 10, but some with less than 2, while those over $600M often have 20+ or more locations.

“With the participation we had in this year’s study, the average has increased over the years, and we’re still seeing a lot of M&A going on, so this is a welcomed improvement,” says Kleoppel.

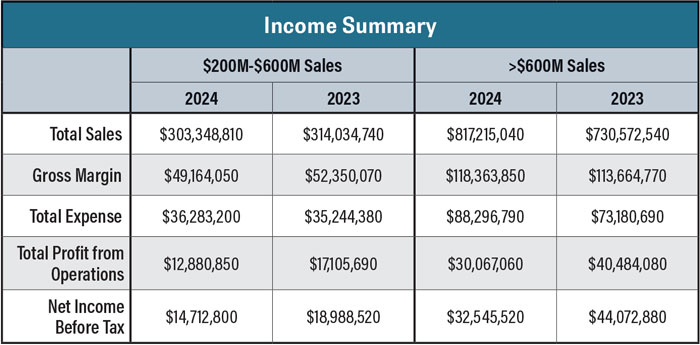

Income Summary Findings & Factors

Total sales volume increased for the >$600M category, with a slight decrease for the $200-$600M categories. The $200M-$600M volume dealer decreased by $10.69M, and the >$600M category increased by $86.64M. The increase in sales volume for the categories mentioned helps create the potential to increase net income and equity, the analysts note. However, they add, both did not increase in net income due to <$50M volume having a decrease in gross margin, and >$600M volume having an increase in total expenses. Of course, they add, equity did increase for both due to the net income added.

Net income as a percentage of sales decreased 1.20% in the $200-$600M category and 2.05% in the >$600M volume category. Source: NAEDA Cost of Doing Business Study 2024 Edition

“The dealers did a decent job in controlling overall operating expenses,” said Kleoppel. There was a slight increase in the dollar amount for the $200M-$600M, and a substantial dollar increase of $15.1M in the >$600M category. Additionally, the report noted that some bigger increases for the >$600M category were in total salaries and benefits, interest expenses, occupancy expenses, depreciation expense, travel/training and advertising.

The authors noted that net income as a percentage of sales decreased in all categories, with a decrease of 1.20% in $200M-$600M, and 2.05% in the >$600M category. The decrease for the latter was a drop of $1.9M in other miscellaneous income.

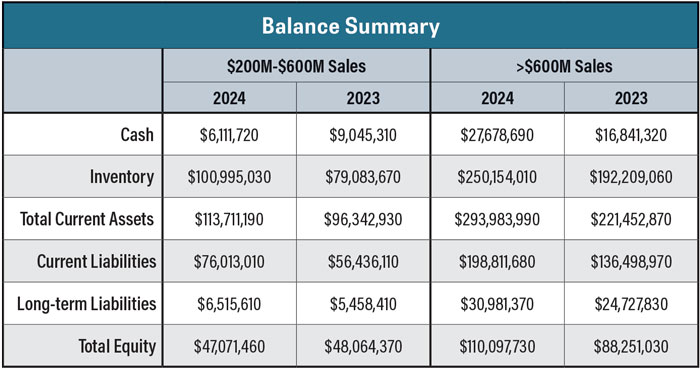

Balance Summary

Areas of focus in the balance summary include: cash; inventory; total current assets; current liabilities; long-term liabilities; and total equity.

Cash increased considerably in the >$600M volume category while inventory levels significanlty increased from the year before in both categories shown. Source: NAEDA Cost of Doing Business Study 2024 Edition

There was significant improvement in some major areas, in two key ways: cash decreased in two categories and increased considerably in the high-volume category with the previous year, notes Kleoppel. Additionally, inventory levels significantly increased from a year ago due to the continued increase in new inventory availability.

New inventory ranged from 40.33% for $200M-$600M, and 41.97% for >$600M as a percent of total assets. All were higher than in the 2023 study. The good news, according to study analysts, is the used inventory percentage ranged from 9.42% to a high of 25.2% for the three categories, which, compared to a year ago, is only a slight increase in each category.

A review of current liabilities increases for the 2 categories in focus showed most of the increase was attributable to the floorplan payables, which the analysts note coincides with the increase in new inventory. Parts inventory ranged from 9.93% to 12.30% of total assets, with the lower percentage being in the >$600M category. Long-term liabilities increased in the two categories, with the most significant increase in dollar amount in the >$600M category, consisting of increases in Notes Payable Other and Notes Payable Shareholders.

Webinar Offers Insights & Analysis on CODB Study

Webinar Offers Insights & Analysis on CODB Study

Representatives from the certified accounting firm which partners with the North American Equipment Dealers Assn. (NAEDA) offered a full analysis of the 2024 NAEDA Cost of Doing Business Study during a Farm Equipment webinar sponsored by Fusable. Click here to watch.

The study also found that the biggest increase was Notes Payable Other, which went from 1.88% to 3.08% of total liabilities and net worth in the >$600M category. Notably, Goodwill increased in the $200M-$600M and >$600M categories, which authors note is a sign mergers and acquisitions are still happening.

Equity increased in dollars, but saw the percentage total decrease due to Floorplan Payable increases from new inventory. Equity percentage ranged from 32.39% to 36.32% for the categories analyzed.

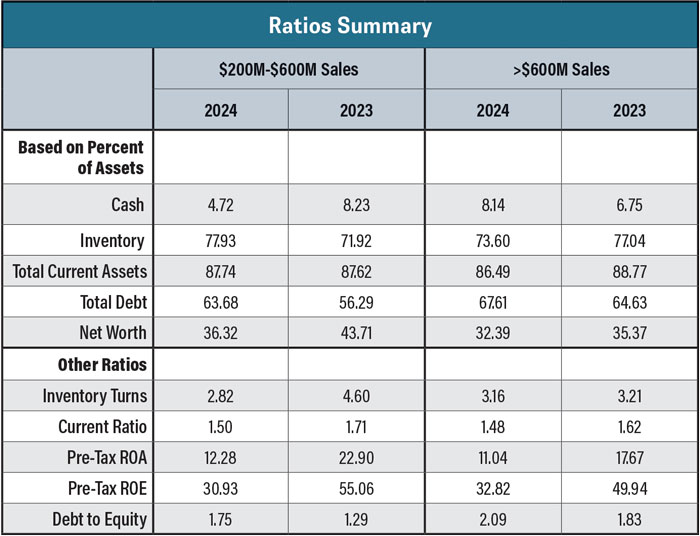

Ratios Summary

The report offers more than 35 pages on revenue, which help dealers easily compare their dealership to what has happened in the industry. Kleoppel says, “Overall, I think the study for 2024 for the year ending 2023 was good ... none of the negatives were dramatic and the net income before tax was healthy.”

The total debt to equity ratio increased for all categories, caused by the increase in debt, mainly due to the rise in inventory. Source: NAEDA Cost of Doing Business Study 2024 Edition

The new and used ratios show a good increase in 2024 from 2023, at 9.4% and 5.5% respectively. Total wholegoods, which were North America numbers, were at 8.1% compared to 2023 at $20,249M. Parts were up 5.9% and service up 2.6%.

Additional findings include:

- Inventory turns decreased in all categories even though sales volume increased in all categories

- The increase in inventory levels was greater than the increase in sales volume, indicated by the decrease in turns.

- The sales volume of $200M-$600M category saw the most decrease in turns, 1.78 lower than the past year.

- The total debt to equity ratio increased for all categories, caused by the increase in debt, mainly due to the rise in inventory.

- Looking at Return on Equity (ROE), the report found: the $200M-$600M volume dealer decreased from 55.06% to 30.93%; the >$600M dealer decreased from 49.94% to 32.82%.

- Each of the dealers had less net income compared to the previous year; total equity increased, resulting in a lower ROE percentage.

In analyzing parts and wholegoods inventory turnover, inventory targets are at least greater than 3 times, noted Kleoppel. The North American average was 2.5 for asset turn and was 2.8 for inventory. By sales volume, the only one greater than 3 times was the over $600 million group. The asset turnover is all assets, and includes even fixed assets.

Observations

- The report’s authors offered key observations in assessing the 2023 data.

- >$600M volume dealers decreased 1.08% in margin, and the $200M-$600M volume dealers decreased 0.46% in margin.

- Inventory turns were 2.82 times for $200M-$600M volume dealers, and 3.16 times for >$600M volume dealers.

- Parts aftermarket absorption was 40.02% for $200M-$600M volume dealers, and 35.95% for >$600M volume dealers

- The >$600M volume dealers’ total inventory in dollars increased close to $57.9M dollars, marking a substantial change from a year ago.

- Total sales volume decreased by $10.7M for the $200M-$600M volume dealers, and increased by $86.6M for the >$600M volume dealers.

- For the $200M-$600M volume dealers, new equipment increased by over $14.7M, and used equipment increased by over $6M.

- Service gross margin percentages: 63.48% for $200M-$600M volume dealers, and 63.45% for the >$600M volume dealers.

- Parts and accessories gross margin percentage was 33.54% for $200M to $600M volume dealers, and for >$600M volume dealers it was 32.51%.