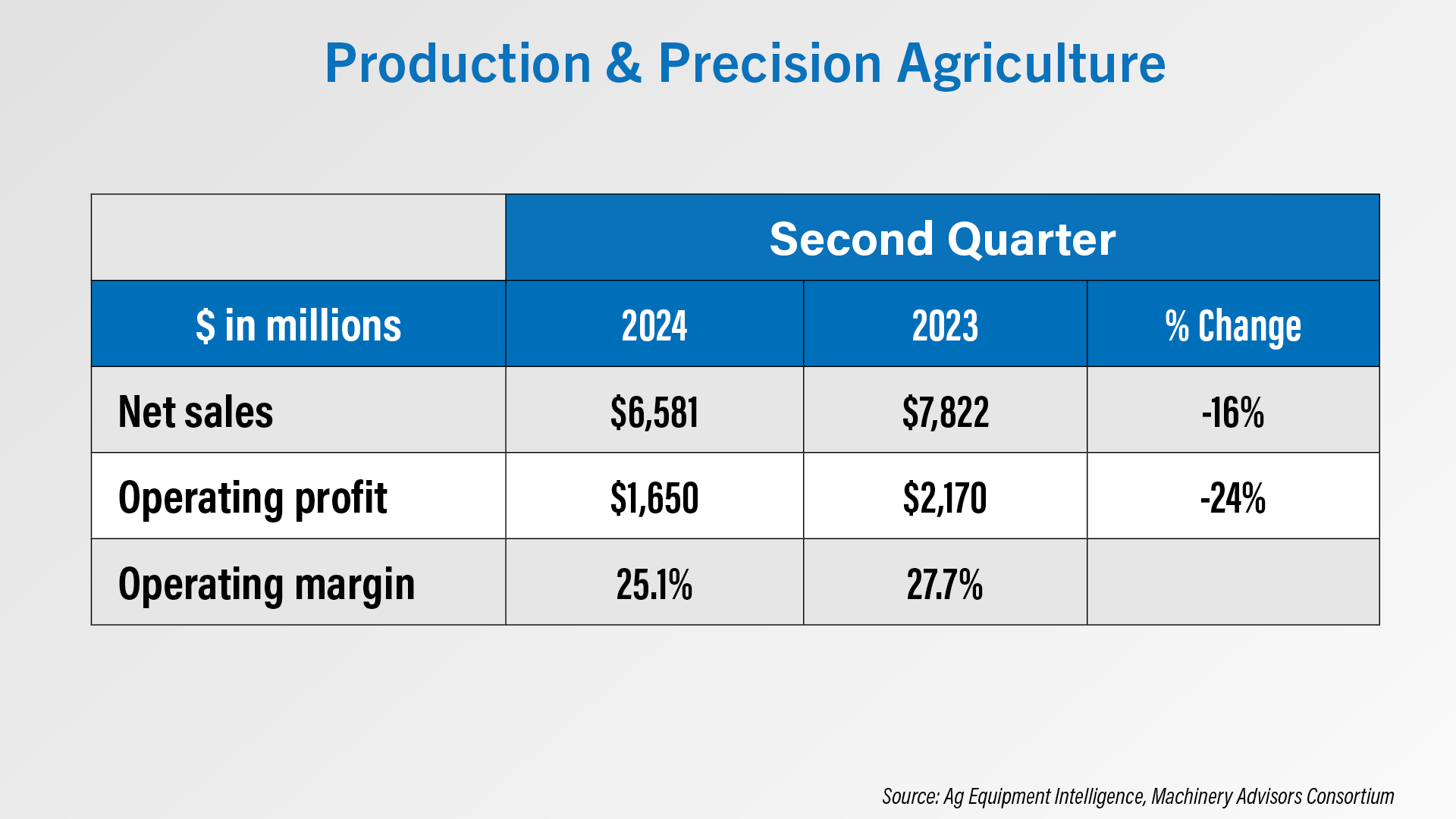

Deere & Co.‘s Production and Precision Ag net sales were down 16% year-over-year for the second quarter. Josh Rohleder, Deere’s manager of investor communications, says the decline is primarily due to lower shipment volumes. That was partially offset by price realization.

Noting that the industry is coming down from a period of high demand, Cory Reed, president of Deere’s Worldwide Agriculture & Turf Division, says historically the industry would be sold to react to that change.

He says:

“Often, we would drive higher levels of field inventory to the detriment of the following years. Within Deere, we're managing this year differently, which is a testament to the fact that both we and our dealers have learned from the past cycles. This is probably best exemplified by our decision to underproduce large tractor retail demand in North America in the back half of the year. We ended 2023 with really low levels of large tractor inventory, but we think it's prudent to drive those levels even lower as we close out our 2024. The key here is that by staying ahead of demand changes, we're giving ourselves the optionality to react most efficiently to whichever way the market moves in the next year.”

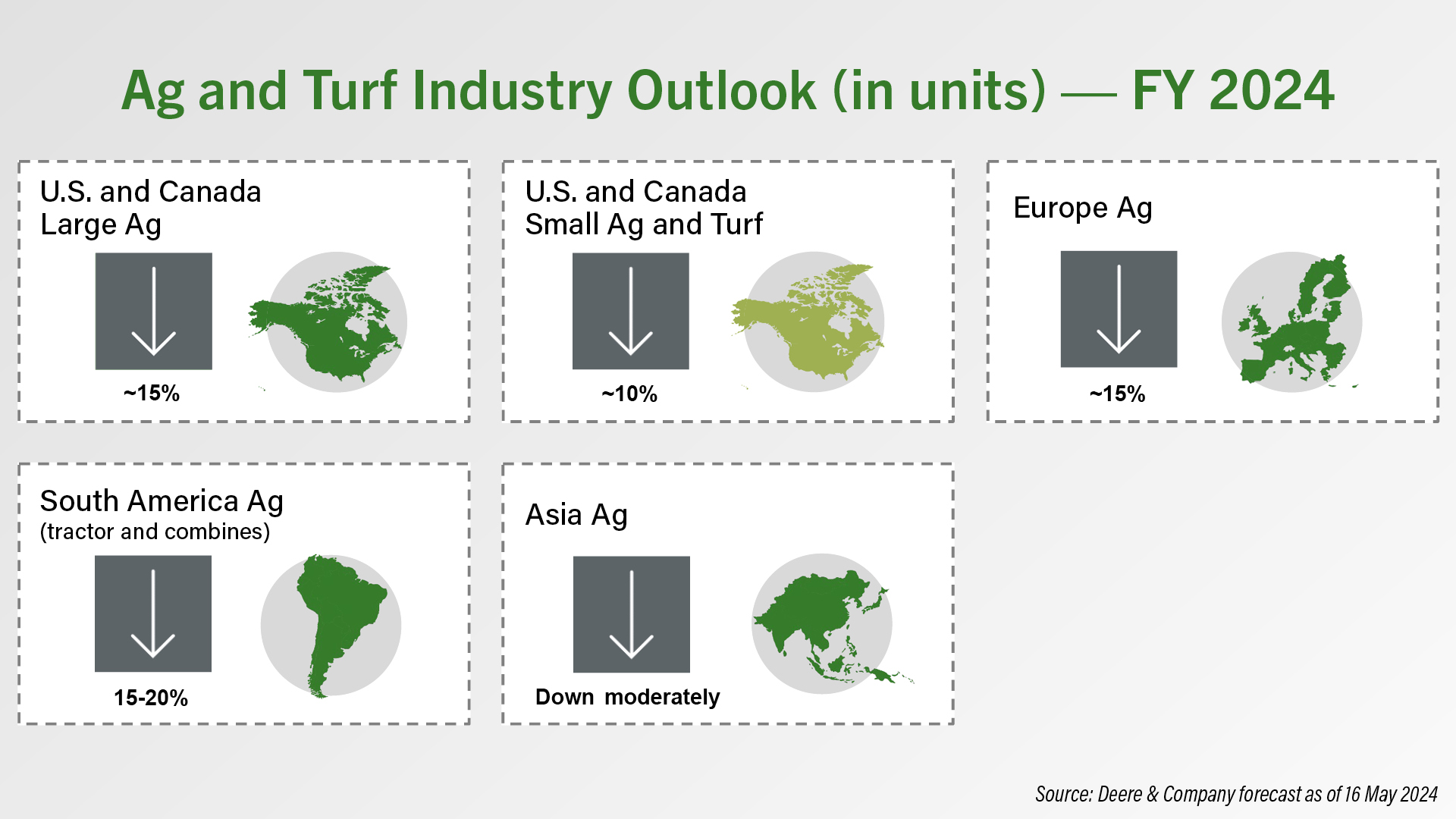

For FY 2024, Deere forecasts large ag sales to be down in all regions.

Rohleder says:

“Across all our major markets, we see continued softening in grower sentiment as the combined impacts of rising global stocks, lower commodity prices, high interest rates, and weather volatility weigh on customer purchase decisions. Amidst this backdrop to rising uncertainty, we're seeing customers exercise greater discretion in their equipment purchases, which is reflected in the changes in our industry guide this quarter.”

“In the U.S. and Canada, Deere now expects large ag equipment sales to be down 15% for the FY 2024. Rohleder says the declines reflect “further demand reduction in the back half of the year, primarily in large tractors.”

He also says increases in used inventory levels, particularly for late model year machines, are impacting purchasing decisions. But, these headwinds are partially offset by fleet fundamental tailwinds, including elevated fleet age, stable farmland values, and strong farmer balance sheets.

Deere expects European large ag sales to be down 15% as well and in South America for sales to be down 15-20%.

Watch the full version of this episode of On The Record