- First quarter consolidated revenue declined 10% on lower industry demand

- First quarter diluted EPS at $0.31; adjusted diluted EPS at $0.33 ($0.35 in the first quarter of 2023)

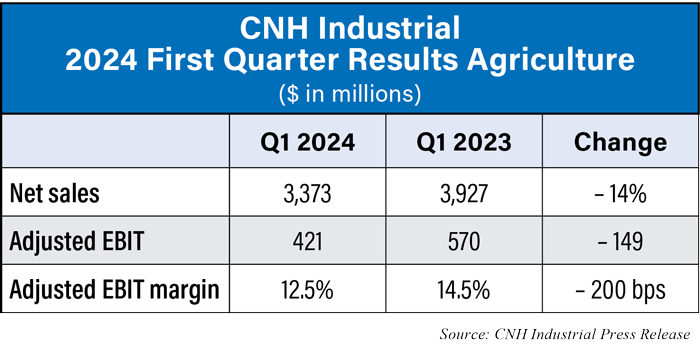

- First quarter Agriculture segment adjusted EBIT margin down 200 bps year-over-year to 12.5%; Construction up 150 bps to 6.7%

- Cost reduction programs on track, helping to mitigate impact of slowing markets

- Full-year guidance updated to reflect lower agriculture industry projections

Basildon, UK — CNH Industrial N.V. (NYSE: CNHI) today reported results for the three months ended March 31, 2024, with net income of $402 million and diluted earnings per share of $0.31 compared with net income of $486 million and diluted earnings per share of $0.35 for the three months ended March 31, 2023. Consolidated revenues were $4.82 billion (down approximately 10% compared to Q1 2023) and Net sales of Industrial Activities were $4.13 billion (down approximately 14% compared to Q1 2023). Net cash used in operating activities was $894 million and Industrial Free Cash Flow absorption was $1,209 million in Q1.

In a note to investors, J.P. Morgan's Tami Zakaria said CNHI's resturcturing program is on track to be completed during Q2. "Previously, CNHI announced an immediate restructuring program to reduce its salaried workforce by 5%," she said. "It also unveiled its plan to right-size its cost structure. These two initiatives are expected to reduce total SG&A by a 10-15% run-rate. CNHI reduced its SG&A expenses by ~12% YoY in 1Q as management imposed strict discipline on discretionary spending, expanded support operations to lower-cost countries, and rationalized back-office operations."

Zakaria also noted that CNHI fell short of decreasing dealer inventory to its desired levels during the quarter. While the company looks to complete dealer inventory cuts during Q2, it could potentially carry into Q3, she said.

“The CNH team navigated a declining market environment in the first quarter, as lower industry demand persisted especially in South America and Europe. Anticipating these headwinds, we are continuing to improve what we can control – production efficiency, disciplined commercial execution, judicious SG&A reductions, and thoughtful product and technology investments. As always, the team is meeting challenges head-on and working diligently to deliver solutions for our customers. I would like to thank our employees and dealers for their unwavering support of the world’s farmers and builders.” — Scott W. Wine, Chief Executive Officer

Net sales of Industrial Activities were $4.13 billion, a decrease of 14% when compared to the corresponding period from the previous year. This decline is mainly due to lower industry demand and dealer inventory management. Price realization continued to be favorable for Agriculture and essentially flat for Construction.

In Q1 2024, Net income was $402 million, with diluted earnings per share of $0.31 ($486 million and $0.35, respectively, in Q1 2023). Adjusted net income was $421 million with adjusted diluted earnings per share of $0.33. In comparison, in Q1 2023, adjusted net income was $475 million with adjusted diluted earnings per share of $0.35.

Gross profit margin of Industrial Activities was 22.7% (24.4% in Q1 2023). The decrease was driven by the Agriculture segment, whose margin was impacted by lower production volumes only partially compensated by price realization and production cost efficiencies. Construction gross profit margin increased across all regions for an aggregate improvement of 150 basis points.

Reported income tax expense was $77 million ($173 million in Q1 2023), and the effective tax rate (ETR) was 19.2% (27.6% in Q1 2023) with an adjusted ETR(3) of 19.4% for the first quarter of 2024 (27.9% in Q1 2023). The Company now forecasts full year 2024 adjusted ETR to be in the range of 24-26%.

Cash flow used in operating activities in the quarter was $894 million ($701 million in Q1 2023). Free cash flow absorption of Industrial Activities was $1,209 million mainly due to seasonal inventory growth. Consolidated third party debt was $27.8 billion as of March 31, 2024 ($27.3 billion as of December 31, 2023).

The Company’s restructuring program continues to progress according to plan, and CNH expects a run rate reduction of 10-15% on total labor and non-labor SG&A expenses. The Company has incurred a total of $78 million of restructuring charges through Q1 2024, of which $53 million was in 2023, and expects to incur up to $200 million in total.

In North America, industry volume was down 15% year-over-year in the first quarter for tractors under 140 HP and was down 2% for tractors over 140 HP; combines were down 17%. In Europe, Middle East and Africa (EMEA), tractor and combine demand was down 15% and down 24%, respectively. South America tractor demand was down 18% and combine demand was down 40% continuing the negative trend of the second half of 2023. Asia Pacific tractor demand was down 12% while combine demand was up 16% in the region as a whole, but down 22% in Australia and New Zealand.

Agriculture

Agriculture net sales decreased for the quarter by 14% to $3.37 billion primarily due to lower industry volume across all regions and dealer inventory management, partially offset by favorable price realization.

Gross profit margin was 23.8% (26.2% in Q1 2023) down 240 bps as a result of lower production volume and unfavorable mix; partially offset by improved price realization, along with lower purchasing and manufacturing costs. Adjusted EBIT decreased to $421 million ($570 million in Q1 2023) driven by the lower volumes, partially offset by improved purchasing and manufacturing costs, and a continued reduction in SG&A expenses. R&D investments accounted for 6.0% of sales (5.3% in Q1 2023). Income from unconsolidated subsidiaries increased $42 million year-over-year. Adjusted EBIT margin was 12.5% (14.5% in Q1 2023).

Global industry volume for construction equipment decreased 1% year-over-year in the first quarter for Heavy construction equipment; Light construction equipment was down 8%. Aggregated demand decreased 14% in EMEA, decreased 6% in North America, decreased 10% in South America and increased 3% in Asia Pacific.

Financial Services

Revenues of Financial Services increased 25% due to favorable volumes and yields across all regions, partially offset by lower used equipment sales due to decreased operating lease maturities.

Net income was $118 million in the first quarter of 2024, an increase of $40 million compared to the same quarter of 2023, primarily due to favorable volumes in all regions, margin improvement in South America, and a favorable effective tax rate due to discrete items in the quarter; partially offset by increased risk costs due to higher aged delinquencies in South America.

The managed portfolio (including unconsolidated joint ventures) was $28.7 billion as of March 31, 2024 (of which retail was 65% and wholesale was 35%), up $4.2 billion compared to March 31, 2023 (up $4.3 billion on a constant currency basis).

At March 31, 2024, the receivables balance greater than 30 days past due as a percentage of receivables was 1.7% (1.4% as of March 31, 2023).

2024 Outlook

The Company forecasts that 2024 global industry retail sales will be lower in both the agriculture and construction equipment markets when compared to 2023. In the aggregate for key markets where the Company competes, CNH previously estimated agriculture industry retail sales to be down between 10-15% but now projects industry volumes down approximately 15%, at the low end of the previous range. Construction equipment industry retail sales are still expected to be down around 10% when compared to 2023.

CNH is continuing its efforts to improve through-cycle margins with its previously announced cost reduction programs focused on product costs and SG&A expenses. Both programs are progressing as planned and are expected to partially offset the impact of the lower industry demand.

As a result of the lower agriculture industry sales projections, the Company is updating its 2024 outlook as follows:

- Agriculture segment net sales(5) down between 11% and 15% year-over-year including currency translation effects (from down 8% to 12% previously)

- Agriculture segment adjusted EBIT margin between 13.5% and 14.5% (from between 14.0% and 15.0% previously)

- Construction segment net sales(5) down between 7% and 11% year-over-year including currency translation effects (unchanged)

- Construction segment adjusted EBIT margin between 5.0% and 6.0% (unchanged)

- Free Cash Flow of Industrial Activities(6) between $1.1 and $1.3 billion (from between $1.2 to $1.4 billion previously)

- Adjusted diluted EPS(6) between $1.45 to $1.55 (from between $1.50 to $1.60 previously)