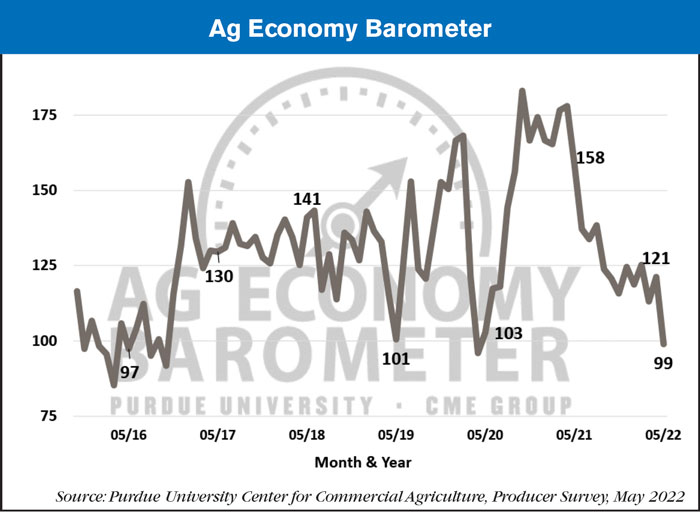

The Purdue University/CME Group Ag Economy Barometer dropped to its lowest level since April 2020, down 22 points in May to a reading of 99. Agricultural producers’ perceptions regarding current conditions on their farms, as well as their future expectations, both weakened this month. The Index of Current Conditions dipped 26 points to a reading of 94, and the Index of Future Expectations fell 21 points to a reading of 101. The Ag Economy Barometer is calculated each month from 400 U.S. agricultural producers’ responses to a telephone survey. This month’s survey was conducted May 16-20.

“Despite strong commodity prices, this month’s weakness in producers’ sentiment appears to be driven by the rapid rise in production costs and uncertainty about where input prices are headed,” said James Mintert, the barometer’s principal investigator and director of Purdue University’s Center for Commercial Agriculture. “That combination is leaving producers very concerned about their farms’ financial performance.”

The Farm Financial Performance Index declined 14 points to a reading of 81 in May. The percentage of producers who expect their farm’s financial performance to worsen in 2022 compared to last year rose from 29% in April to 38% in May. Over the course of the last 13 months, the Farm Financial Performance Index has fallen 41% below its life-of-survey high of 138 set in April 2021.

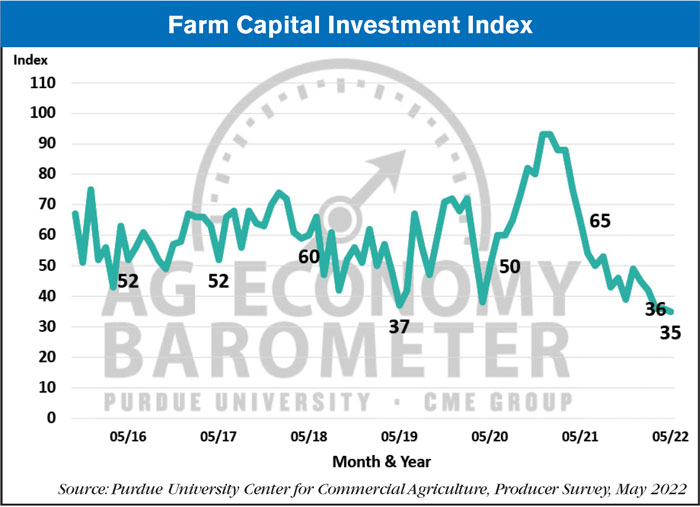

The Farm Capital Investment Index drifted to an all-time low in May and is down 30 points from this same time last year. In the May survey, only 13% of respondents said this is a good time to make large investments in their operation, while 78% said they viewed it as a bad time to invest in things like machinery and buildings. Half of the producers in this month’s survey said their machinery purchase plans were impacted by low farm machinery inventory levels, up from 41% in the April survey, suggesting that supply chain issues are at least partly responsible for the ongoing weakness in the capital investment index.

Higher input costs remain a top concern for producers with 44% of those surveyed choosing it as the biggest concern facing their farming operation in the coming year. Additionally, 57% of producers said they expect a 30% or more rise in prices paid for farm inputs in 2022 compared with prices paid last year. The May survey also asked producers about their expectations for input costs in 2023 compared to 2022 with nearly 39% of producers indicating they expect an additional cost increase of 10% or more in the coming year.

In response to a Biden administration policy proposal for a $10 per acre wheat/double-crop soybean crop insurance subsidy, this month’s survey asked respondents if the subsidy would encourage them to plant more wheat in fall 2022 than would otherwise be the case. Among producers who have employed a wheat/double-crop soybean rotation in the past, just over one in five (22%) said it would encourage them to plant more wheat. Among producers who have not followed a wheat/double-crop soybean rotation in the past, just one out of 10 producers said the insurance subsidy would encourage them to plant more wheat this fall.

Lastly, farmers remain optimistic toward farmland values. The Short-Term Farmland Value Expectations Index, based upon producers’ 12-month outlook, rose 1 point to a reading of 145. Meanwhile, the Long-Term Farmland Value Expectations Index, based upon producers’ farmland outlook over the upcoming five years, rose 8 points in May to a reading of 149. In a follow-up question, respondents who expect farmland values to rise over the next five years were asked the main reason they expect values to rise. Over the past few months that this question has been posed, respondents have consistently chosen non-farm investor demand as the top reason, followed closely by inflation.

For a more in-depth look at the survey results, head to Ag Equipment Intelligence.